Hello readers! We are back with another knowledgeable article to help you in establishing a successful career as a Certified Public Accountant (CPA).

REG is one of the four parts of the CPA exam that you have to pass to acquire your CPA license.

However, the REG section of the CPA exam is a difficult one based majorly on federal taxation. This is why you need to learn all it takes to pass the exam.

By the end of this article, you will know the entire REG CPA format, study procedures, and useful tips to ace your exam.

Here is what we will cover in this article:

So, let us not waste your time and delve straight into the pool of information that will help you surface as a professionally licensed CPA in no time.

About the REG CPA Exam

There is nothing as scary as failing an exam that puts your career at stake.

The job market is in-demand for professional CPAs. They tend to be super-efficient and skillful when it comes to accounting, handling tax legalities, financial accounting, auditing, and representing the firm financials based on IRS standards.

Even though CPA is considered a tough exam, there is no reason why you shouldn’t attempt it and give it your best shot.

The first step to acing the exam is to learn about it. Many of the candidates make the mistake of not researching the REG exam; hence, the outcomes are undesirable.

REG is a Regulation CPA exam and is a part of this exam alongside the three others- BEC, AUD, and FAR.

To qualify as a CPA, it is essential to pass all four of these sections.

The REG Exam comprises federal taxation, business law, and ethics. Even though each topic consists of a variety of sub-topics and is quite expansive, the major chunk of the paper is based on federal laws.

The federal tax procedures and all tax-related stuff make up more than 50 percent of the entire REG exam section.

The key is to prepare for the exam with utmost dedication. While business law and ethics do need your attention, invest your energy and study time smartly to understand, memorize and apply the concepts of taxation and various tax laws.

Pass Rate

Exams can be draining, and if it is CPA that you are taking, it is easy to get cold feet even before you begin preparing for it.

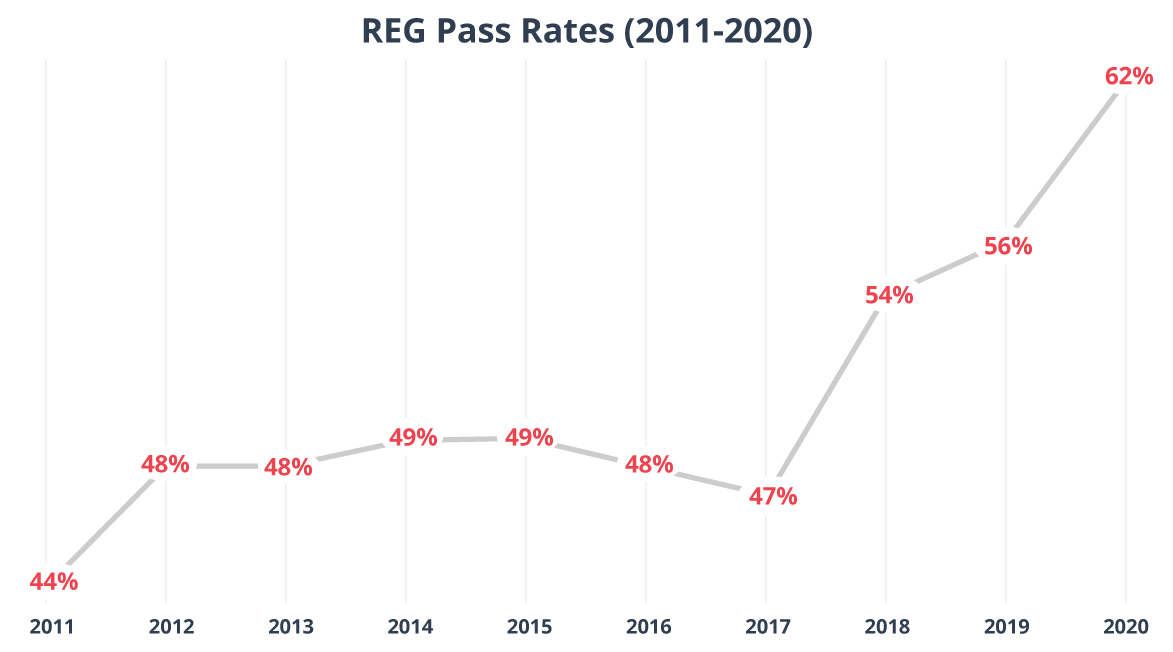

During the years, REG has witnessed the second highest pass rate after the BEC section of the CPA exam.

According to the statistical data by AICPA (the American Institute of Certified Public Accountants), the pass rate percentage has significantly grown from a mere 44% to 62% in the last decade.

To give you a clear heads up on the four sections of the CPA exam, here are the recent pass rates for each of them:

- BEC- 62.84%

- REG- 59.03%

- AUD- 49.7%

- FAR- 44.7%

As per AICPA, generally, around 50% of the total candidates pass the CPA exam on average, every year.

One of the biggest reasons that the passing score for REG has spiked may be due to the abundance of CPA review courses, and online study guides alongside informative articles like this one.

Even if you do not pass the CPA exam at first, you can always give a second attempt. It is recommended to appear for only one or two sections at one time to get better results.

As they say, never put all your eggs in one basket. Studying for four sections of CPA altogether can be extremely difficult and lower your chances of passing the exam in one go.

To learn about the format and reach an informed decision about how you want to sit for the exam.

REG CPA Exam – The Format

What if we tell you that we know what is going to come up in your exam? You would want to know all about it, right.

Well, we are just about to do that.

Not that we know about the questions or their answers but we can help you with learning about the format and content of the exam to study accordingly.

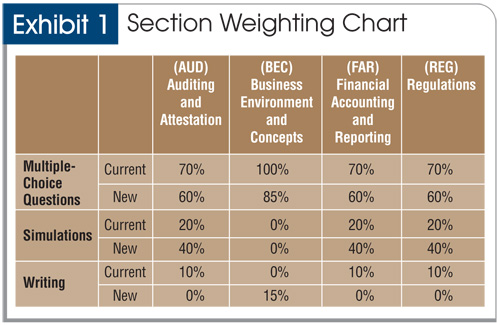

The REG section of CPA has a structural exam format based on five parts, also known as testlets.

The testlets cover two types of questions, multiple-choice questions (MCQs) and task-based simulations (TBS). And these are further subdivided into the operational and the pretest questions.

Multiple-choice Questions – MCQ testlets have one question- one-liner or a paragraph with four suggested answers. Out of the total 76 MCQs in the REG exam, 12 of them are a part of the REG pre-test exam and do not account for the candidate’ score or the pass rate

Task-Based Simulations – While MCQs give you the opportunity to skim through your brain and select the answer you think is right, TBS are more practical, real-life case study questionnaires. The candidate has to type in or write down the answers applying the concepts and principles they have learned. These questions can range from research-based to tax laws findings and calculation tax allocations.

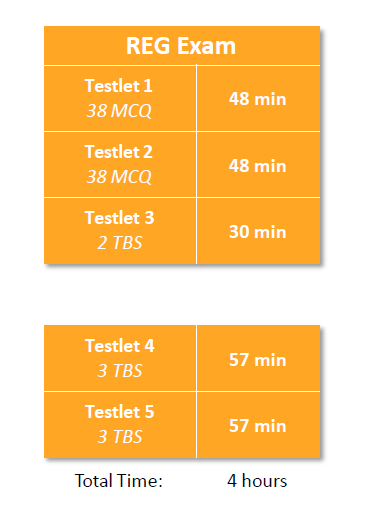

Here is what the format looks like:

- Testlet 1: 38 MCQa

- Testlet 2: 38 MCQs

- Testlet 3: 2 TBSs

- Testlet 4: 3 TBSs

- Testlet 5: 3 TBSs

So, you will have to prepare for a total of 84 questions covering the entire REG course, as the questions tend to be thorough.

- Before you appear for the actual exam, as per AICPA you can give the REGCPA exam pretest questions with a total of 12 Multiple Choice Questions (MCQs) and 1 Task-Based Simulation (TBS).

The purpose behind this is to assess your performance and see where you stand. You will not be scored for this pre-test, it just provides AICPA with information and scoring data for later use.

- The operational questions are the one you appear for in the actual exam.

Apart from an excellent grip on course content, it is essential to manage the exam in the allocated time.

Time Allocation for REG Exam

- REG pretest:

The pre-exam that the candidates appear for right before the actual exam lasts for a total of 10 minutes. It has two parts, therefore the candidate gets 5 minutes for each section.

- REG CPA Exam:

REG is a four hours long exam, with only one 15-minute break allocated between the first and the second TBS testlets.

Worry not, the candidate can leverage two optional breaks one after the first and one after the second MCQ testlets. However, the timer does not stop for these breaks, they are deducted from your valuable exam minutes.

During the exam, the candidates need to keep an eye on the time relevant to their pace with solving the questions.

Practice exam questions and review courses are a great way to manage the allocated time on the actual exam.

Moreover, practice prepares you to face difficult questions, effortlessly in the exam.

The exam blueprints can help you prepare fail-proof mental notes and time tackling methods to finish each REG section before the timer stops and pass with flying colors.

The candidate can finish as early as they want, and they could- there is no hard rule to stick to the four-hour deadline.

Here are a few tips to help you manage your time efficiently:

- Do not allocate the same amount of time to each question. If you can answer a question quickly, do it. Use that extra time on the questions you get stuck in

- Do not waste your time settling on the answer to a question. If you have already made an educated guess, it will take time studying answer, flag the question, and solve others. You can utilize the saved time and review the flagged question once you are done with the others

- Practice enough questions before the exams so that you get a grip on your pace and know how to read, understand and answer the question in the given time

To manage the time more efficiently, learn about the exam content. Align the two together to ensure your win on the exam day.

REG Exam Content and Grading

As a kid, the topic that you were least interested in was most likely to appear in the exam and it becomes a complete nightmare.

To increase the possibility of your passing on the exam, it is essential to prepare on all grounds.

AICPA is responsible for publishing the REG CPA exam blueprints to specify all content areas to the candidate. Amongst the three major areas of REG, federal taxation is the dominant one.

AICPA REG Blueprint

| Content Area | Percentage of Questions |

| Ethics, Responsibilities, and Federal Tax Procedures | 10-20% |

| Business Law | 10-20% |

| Federal Taxation of Property Transactions | 12-22% |

| Federal Taxation of Individuals- Planning strategies and tax preparation | 15-25% |

| Federal Taxation of Entities- Planning strategies and tax preparation | 28-38% |

Even though these blueprints provide detailed data on each topic, it would be difficult to invest so much time on them while you can study instead.

Here is how expansive each content area is:

Ethics, Professional Responsibilities, and Federal Tax Procedures

- Ethics and responsibilities in tax practice

- Regulations of governing practice before the IRS

- Procedures of federal tax

- Appeals, judicial process and audits

- Internal revenue code and regulations in relevance to tax returns

- Licensing and disciplinary systems

- Penalties related to taxpayers

- Substantiation and disclosure of tax positions

- Authoritative hierarchy

- Legal duties and professional responsibilities

- Common law duties and liabilities to clients as well as the third parties

- Privileged communications, confidentiality, and privacy acts

Business Law

- Agency

- Authority of agents and principles

- formation

- Duties and liabilities of agents and principles

- Performance

- Remedies, discharge and breach

- Relationship between debtor-creditor

- Contracts

- Rights, duties and liabilities of debtors, creditors and guarantors

- Bankruptcy and insolvency

- Secured transactions

- Business structure

- Government regulation of business

- Federal securities regulation

- Other federal laws and regulations

- Selection and formation of business entity and related operation and termination

- Rights, duties, legal obligations and authority of owners and management

Federal Taxation of Property Transactions

- Acquisition and disposition of assets

- Dispositions- taxable and nontaxable

- Basis and holding period of assets

- Taxation- Gift and Estate

- Gains, losses, and netting process- the amount and character of each

- Related party transactions

- Cost recovery such as depreciation, depletion, amortization

- Taxable estate determination

- Transfers eligible to gift tax

- Gift tax annual exclusion and deductions

Federal Taxation of Individuals

- Gross income (inclusions and exclusions)

- Loss limitations

- Alternative minimum tax

- Reporting items from pass-through entities

- Computation of credits and taxes

- Gross income and taxable income- adjustments and deductions

- Losses accounting for passive activity

Federal Taxation of Entities

- Tax treatment of formation and liquidation of business entities

- Computations of tax liability, credits allowance, and taxable income

- Book and tax income (differences)

- Limitations for capital loss and net operational losses

- C corporations

- S corporations

- Entity/owner transactions covering the contributions, loans and distributions

- Tax returns consolidation

- Issues of multijurisdictional tax

Candidates can find it difficult to comprehend the content for the REG exam. Nevertheless, you can take a review course using the blueprints alongside guidance to save time.

There are several reliable review courses available, including:

- Becker CPA review course

- Gleim CPA review course

- Roger CPA review course

Every candidate’s skill level is tested with the REG course content areas.

Here is the content allocation for each skill:

- Level I, 25-35%:It assess how well the candidate remembers and understands the content areas

- Level II, 35-45%: The application of the concepts and the content

- Level III, 25-35%: The analysis of the content

The TBS testlets of the exams are more likely to assess the candidate’s ability for application and analysis during the REG exam.

REG Grading Process

As per AICPA, the REG exam has two levels of difficulty and the candidate’s scores are derived 50% from the MCQ testlets and 50% from the TBS testlets.

You may score a total of 75 or higher to pass the REG

The AICPA CPA pretest questions that align with the standard of the AICPA, are added as the operational questions in the actual exam. A candidate’s performance on the pretest also determines the difficulty level for the testlets and grading.

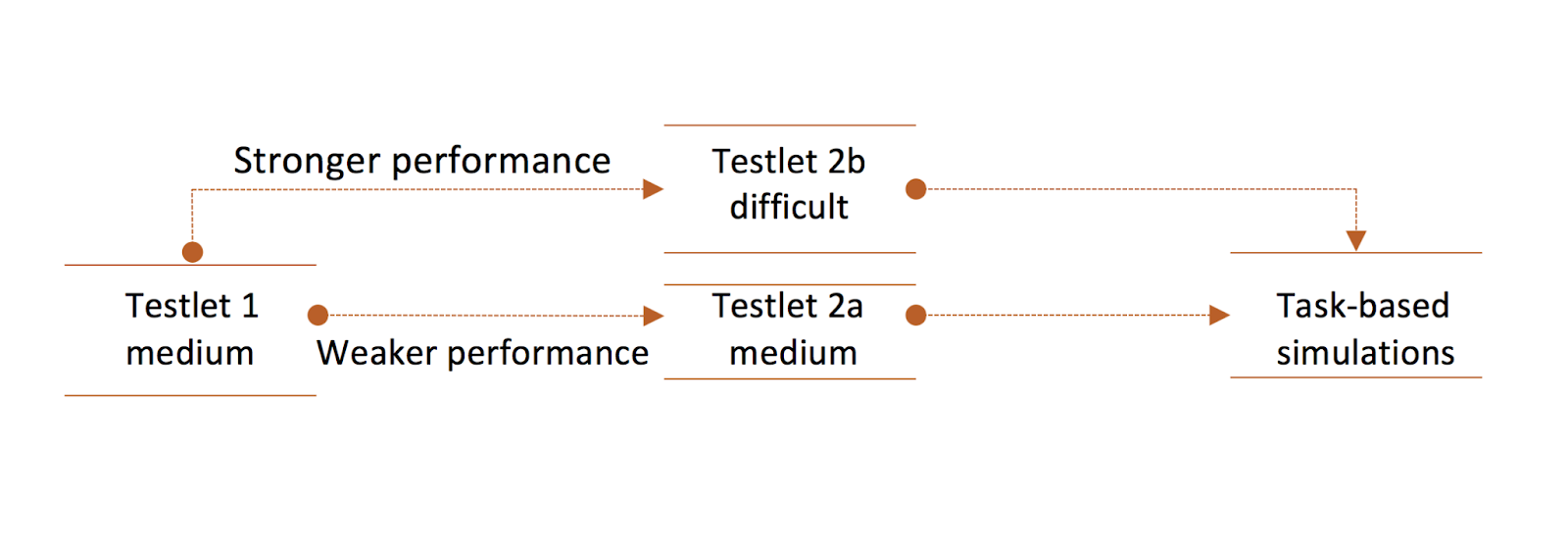

The difficulty level for the Multiple Choice Question testlets can go from “medium” to “difficult”.

The way you perform on each testlet determines the difficulty for the next one. If you perform well on the first one, the next MCQ testlet is going to be a “difficult” one. However, if you do not perform at par, the next testlet will be a “medium”.

For the Task-based simulations, testlets are pre-set, the difficulty level does not change with your performance.

However, you can score partial credits or receive non-research-based TBS testlets if you perform well.

The level of difficulty determines the grading for the exam. Harder questions signify more points.

The better you perform, the higher you score.

There are no penalties or negative markings for the wrong answers. Therefore, do not leave the answer blank, take a guess.

The worst that can happen is you will get a zero if it goes wrong, which you get for leaving it black otherwise. But if you get it right, you get a step closer to passing your exam.

Now that you are familiar with the format, content, and grading system, it is high time to prepare for your exam on the basis of what you know.

Study Tips on REG Preparation

REG focuses majorly on the tax-related topics that can be difficult for the candidates to prepare for.

Here are some useful CPA REG exam tips that can help you to play to your strengths in the REG exam.

Decide when to take REG – Once you take the first CPA exam, you have an 18-month window to pass all fours sections. If you have prior experience as a tax accountant or have knowledge about the tax laws you would probably not require much time to prepare for REG.

Therefore, it would be a good idea to save REG for the last exam as you can prepare for it in less time. However, if you find taxation difficult with all those audits and financial statements confusing you, make REG your first exam.

Because there is no limited study time and you can maximize the chances of passing REG.

Moreover, if you are not good with the concepts of tax and its applications, it would be good to appear for REG after you have done the FAR section of the CPA exam.

Even though FAR is the toughest of all, it helps you prepare for REG as well, this is because of many concepts and content areas for the two overlapping.

Learn Excel– During the CPA exam, you would be dealing with a lot of numbers that will require expertise in spreadsheet tools. The good news is that CPA uses Microsoft Excel as the spreadsheet tool.

Therefore, you can become an expert in Excel by learning handy tips to create, calculate and execute functions. If you do not know how to use Excel, better learn it because you can leverage the tool in all testlets.

Know your way with REG – Practice questions and exams can help you a great deal with understanding the nature of tax questions in the REG exam. It is essential that you take your time to understand the regulation simulations, as they account for a more portion of the exam.

Practice managing time allocation, get familiar with the concepts and their applications. Before you answer the simulation question, ensure that you fully understand what it is asking for.

Oftentimes, candidates cannot decipher the research-based questions and answer them wrongly.

Therefore, give enough time to get to know and correctly answer them, but not too much so that you have no time left for others.

Use up-to-date and efficient study materials – REG updates the tax laws, as it did with the Tax Cuts and Jobs Act in 2019 which influenced a change in the entire study and preparation method.

Certain CPA review courses like Surgent, Gleim, or Becker provide free and unlimited access to the most recent updates in any of the CPA exam sections. You can keep track of your study guide and ensure that you have the right study materials.

Every candidate has a different learning pace. Make a schedule, select the study materials, and the review course that aligns with your mind and learning capabilities.

Allocate your study time smartly to the content areas: As Federal Taxation Procedures dominate the REG exam (55-85%), spend more time preparing for it.

Learn about the concepts and application of tax law procedures for transactions, individuals, and entities.

However, this does not mean that you neglect the other content areas of Business Law, Ethics, and Professional Responsibilities because you never know what is going to show up in the exam.

Do not forget to take notes- Even though REG tests your memorization skills- the entire exam is based on how well you remember the tax laws, facts, and figures.

So, while studying, take notes to enhance your memory.

Writing down the things you are trying to memorize can help you in many ways.

Learn to apply the concepts practically- Memorizing and understanding the content is essential, however, if you fail to analyze and apply the knowledge practically, you might have to reappear for the exam.

Alongside studying the relevant provisions, learn the ways to apply them in the exam.

Practice makes perfect– solve as many practice questions, especially the MCQs as you can. Search the internet, skim through the review courses and get a hang of every last REG practice question you find.

Your practice will only make you better.

Have a plan! Note down all the tips, gather the study material, familiarize yourself with the REG format and study smartly. The combination of knowledge and practice is what it takes to put your best foot forward and pass your way through the CPA exam!

Key Takeaway

There is no magic trick to passing your exams if you are not willing to put in the effort and time.

CPA is known to be one of the toughest exams with an average pass rate of only 50%. So, if you want to be in that 50% learn everything you can about the REG CPA exam- the format, content, and the study procedure.

Once you pass the exam and acquire the CPA license, a highly lucrative job market awaits you.

The exam is only as challenging as you anticipate. Do not overwhelm yourself, look for the right resources, develop a routine, practice as much as you can and treat yourself to the wins – keep yourself motivated!